Year-to-Date 2024 Returns (as of 6/30/2024)

Source: Morningstar, 6/28/2024. U.S. Large Cap Stocks, S&P 500. U.S. Small Cap Stocks, Russell 2000. International Developed Stocks, MSCI EAFE. Emerging Market Stocks, MSCI EM. U.S. Short Term Bonds, Bloomberg U.S. Gov’t 1-3 Year. U.S. Aggregate Bonds, Bloomberg U.S. AG Bond. U.S. Municipal Bonds, Bloomberg Municipal Bond 3+ Year. Global Bonds, Bloomberg Global AG Bond. This chart shows year-to-date 2024 returns (as of 6/28/2024) for U.S. Large-Cap Stocks (15.29%), U.S. Small-Cap Stocks (1.73%), International Developed Stocks (5.34%), Emerging Market Stocks (7.49%), U.S. Short-Term Bonds (1.20%), U.S. Aggregate Bonds (-0.71%), U.S. Municipal Bonds (-0.54%) and Global Bonds (-3.16%).

A seasonally suiting metaphor to describe markets is the packaged boxes of fireworks only available to buy this time of year. (It’s the one day of the year when my kids can’t wait for the sun to set, and the one day we completely capitulate in the high stakes negotiation of a reasonable bedtime with our 5-year-old.) The fireworks box comes with a few big boomers, a lot of small poppers, some I’d rather not spend any money on and inevitably a few duds. The problem is you can’t predict which ones will be duds. It’s totally impossible to determine how they’ll turn out just from looking at the labels, size or fancy packaging. Also, they’re dangerous if mishandled but rewarding if prudently managed. Markets are the exact same. Over the long-term a best practice is to buy the entire box. Don’t try to pick the boomers or the duds as often they are one in the same, like the last time we saw similar market dynamics manifest themselves. Even the big boomers don’t boom forever. The fireworks that boomed at the turn of the millennium are eerily similar to market returns through the first half of 2024.

The biggest domestic stocks are doing great while everything else is relatively disappointing or an outright dud. In the excitement, Nvidia zoomed to the top — and a great thing is that you probably own a lot of it if you are broadly diversified and own many of the largest indexes, like the S&P 500.

This broad diversification works beautifully over time, as you get to participate in the exciting names as they grow and grow but you’re not beholden to them when they inevitably fade from glory. This concept is so important, because the names always change. There’s always a different hot dot investment, and inevitably there’s a change in who it is. Oftentimes, names will grow and come to dominate only to then disappear. Don’t bet on who’ll be the king of the jungle — just own the jungle.

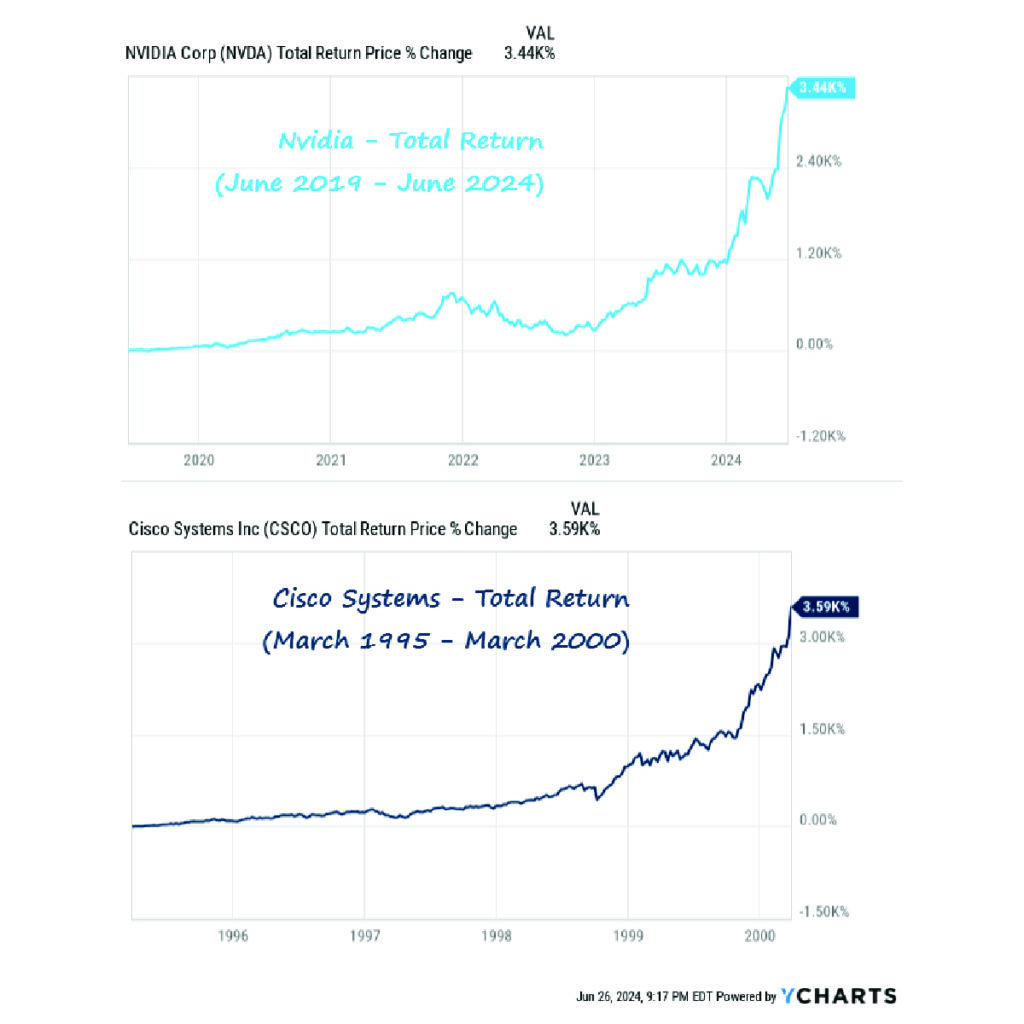

So far, the resemblance between what’s happening with Nvidia today and what happened with Cisco during the last bout of unbridled market excitement around new technology is uncanny.

The above charts show the total return price % change for Nvidia Corp (NVDA) between June 2019 and June 2024 and for Cisco Systems Inc. (CSCO) between March 1995 and March 2000.

Many thought the world was ending with Y2K and fortunately it didn’t; Cisco’s dominance absolutely did though, and those who chased returns did see a portfolio end-of-days of sorts.

Cisco lost 90% when the tides turned, and it’s still worth significantly less today! More useful, though, is the graph showing the extraordinarily difficult decade that followed for growth stocks and the S&P 500 as a whole. As graphed, the entire first decade of the new millennium was a lost one for large domestic growth stocks (down 33%) and large U.S. stocks in general. However, it wasn’t a lost decade for investing overall, as the other elements within a well-diversified portfolio performed much better. Boring bonds made 85%, small company stocks did the same and emerging markets returned more than 160%!

Source: YCharts

Unfortunately, many investors made a terribly mistimed decision, chasing the hot dot of emerging markets at the exact wrong time. Greed-driven decision-making is just as cancerous for prudent long-term investing as are fear-based overreactions.

In the early 2000s, the investment siren song was saying you MUST invest in the BRIC economies (Brazil, Russia, India and China). All these different asset classes deserve a place in a well-diversified portfolio but should never be chased. The vacuum cleaner salesmen of Wall Street who pushed emerging markets then are pushing technology stocks now. Please just tune out the noise and don’t answer the door. (It’s worth noting that no disrespect is meant toward vacuum cleaner salesmen — their products work much better than those of the Wall Street variety, typically.) Unfortunately, the messes made for investors by Wall Street salesmen have often been very difficult to clean up.

Continuing on our “ye beware of fortunetellers” theme, the current state of interest rates and their impact on the consumer (who, in turn, drives the vast majority of overall economic activity) needs to be highlighted. Some of the most influential people in the world (members of the Federal Reserve, who dictate all interest rates) got it wrong to start 2024 when they proclaimed three interest rate reductions in 2024. However, the experts who make their livelihood analyzing influential people in the world got it even more wrong when they called for six or seven interest rate reductions this year. So far, there have been a whopping zero interest rate cuts in 2024.

This discrepancy between projections and reality just further reinforces one of our core beliefs: guessing the short-term trajectory of anything is just that — a total guess. The Federal Reserve may as well have said, “we have a crystal ball to foretell the future,” and these Wall Street strategists still would have said “we analyze a lot of crystal balls, so we know even better what the crystal ball will say.” Again, don’t answer the door when they come knocking.

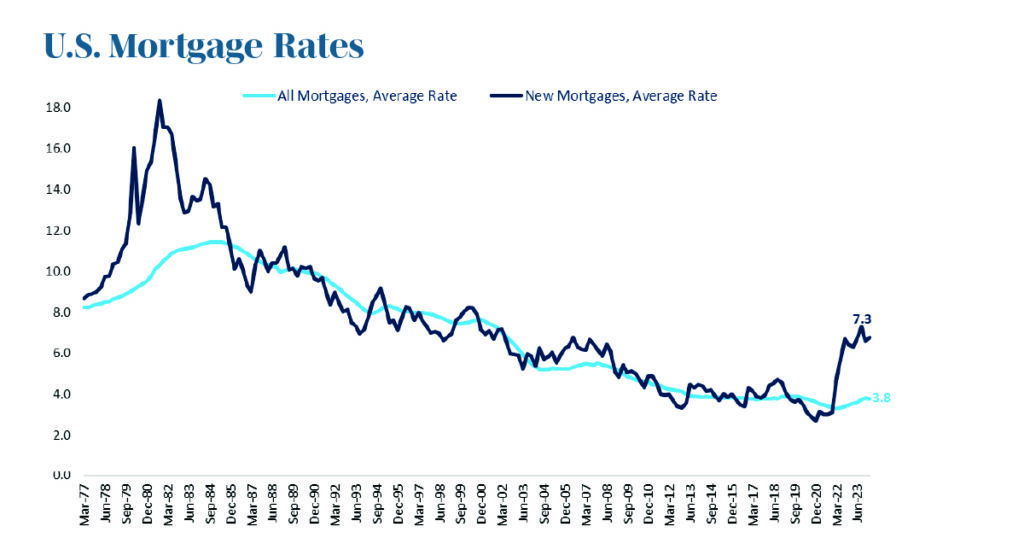

Higher interest rates than markets anticipated and the impact they have on consumers often only tell one side of the story. Yes, as graphed, too many Americans carry credit card debt and are suffering from these higher rates, but a full one-third of households have no debt at all.

Source: Bloomberg

Mortgage rates are higher, but nearly one-half of all homes have no mortgage at all! Looking at mortgage rates in total shows that while new mortgage rates are above 7%, on average, all mortgages are currently at 3.8% — a far cry from the more than 10% average rate and 17% new rate my parents paid in 1979 for the house they still live in today.

Source: BEA, FRED. The above chart shows the average rate of all U.S. mortgages and the average rate for all new U.S. mortgages from March 1977 through June 2023. The lines often move together between December 1985 and March 2022. Prior to December 1985 and after March 2022, the average rate for all new U.S. mortgages was noticeably higher than the average rate for all mortgages.

The point of this isn’t to make people who locked in lower rates feel better about themselves. It’s also not so that I can have the chance to say hi to my folks (I love you very much, Mom and Dad!). Rather, the point is to highlight a large swath of consumers that are not impacted by — or are actually benefitting from — higher interest rates.

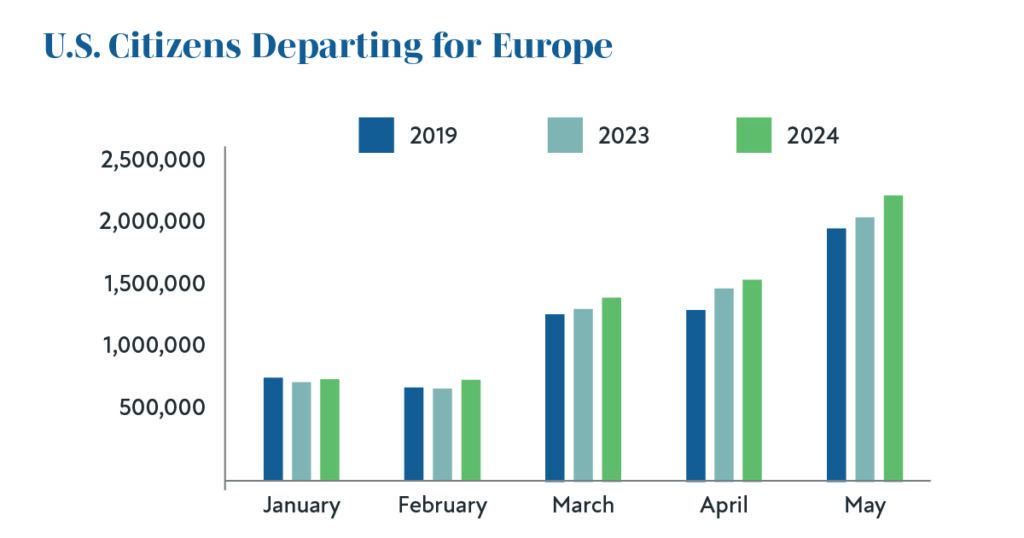

Consumers are still spending, which is helping drive the economy forward. Because we’re in the season of summer holiday travel, we need look no further than record levels of Americans traveling abroad.

Source: International Trade Administration. The above chart shows the amount of U.S. citizens departing for Europe in January, February, March, April and May of 2019, 2023 and 2024.

Individual investors generated a record $1.7 trillion of income from investments to begin 2024. Corporations also benefitted as U.S. companies added to their cash accounts, sending holdings to a record $4.11 trillion (a resilient economy and relatively high interest rates helped boost returns).

It’s great that investors are earning more in their savings accounts and from bonds, but don’t let these higher rates fool you; you are rewarded more over the long run for being an owner (stocks) than for being a lender (bonds) — and cash underperforms 100% of the time over the long term.

Cash, bonds and stock can all serve a purpose in a well-diversified portfolio, but even those nearing or in retirement hopefully have a long time horizon ahead of them to justify the benefits of leaning more heavily toward equity ownership. Household net worths being near all-time highs, on average, not only benefits overall economic activity but also reinforces the long-term benefits of broad ownership and the prosperity it slowly manifests.

The times we live in have always been — and hopefully always will be — exciting, but they’re also fraught with things to worry about. Political concerns and market innovations to mesmerize are as old as politics and the markets themselves, but the benefit of tuning out this noise in prudent investment decision-making is just as timeless. Leave the booming noise to the fireworks.